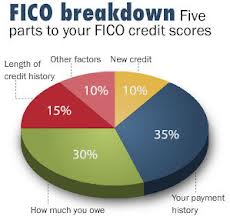

The system of credit reports and scores in Canada is very similar to that in the USA, with two of the same reporting agencies reporting: Equifax and TransUnion. Both countries also use the FICO scoring system which is the abbreviation for Fair, Isaac and Company, a Public Traded company that developed a credit scoring system which is determined on ‘risk assessment’. According to Equifax’s ScorePower Report, FICO scores range between 300 (high risk) and 900 (low risk).

SO what does this mean?

Well, your credit score can be used to determine your credit worthiness and having a calculated score makes it easier for creditors to determine if you are high risk or low risk. You may be the nicest person in the world, but its your FICO that ultimately decides your credit risk score.

High risk FICO scores: 599 and under will have apparent credit issues or past credit problems, these can be collections, late payments plus defaulting on credit cards and loans. These scores will typically deny you bank credit cards and loans and you would be looking at the high interest equity or secured loan market.

Fair risk FICO credit scores: 600-700 will open more options for credit. It still may be difficult to get a bank credit card or loan, but lower interest credit cards and loans from private lenders are available. These scores typically do not require a security.

Low risk FICO credit scores: 701 to 900. I FICO score in this range will give you the best options available; especially scores over 800. These scores are considered low risk which means you don’t have a high debt to credit ration, you pay your bills on time and you have no collection or credit issues. It also means that you have likely had credit established for quite a few years.

If you want to find out what your credit score, you can do so either online or by mail by contacting Canada’s two credit reporting bureaus: Equifax TransUnion

{kind=link}

Recent Comments